Emerging Markets (EM) have long been associated with high growth potential, but also equally high volatility. As we move into 2026, however, it is crucial to consider how the EM landscape is shifting. Structural changes, shifting regional dynamics, and growing divergence within EM means investors need to rethink their approach towards EM exposure.

Decades ago, EM was largely associated with commodities, infrastructure development, and export-led growth. While still important, these are no longer the primary forces shaping EM performance. Today’s EM is increasingly driven by domestic consumption, technology adoption, and expanding middle-class demand.

Not all Emerging Markets Are the Same

That said, it is important to recognise that emerging markets are far from uniform. “EM” is really an umbrella term for regions with very different economic environments:

- Asia: Greater focus on growth and innovation, including areas like e-commerce, IT services, and advanced manufacturing. But it’s highly nuanced: China, India, and Southeast Asia perform very differently due to policies, domestic demand, and political environment.

- Latin America: Performance heavily tied to global demand for copper, lithium, oil, and agricultural products. Political cycles create volatility, affecting fiscal policy and investor confidence. Some countries like Mexica benefit from nearshoring, while others remain rife with structural challenges. Picking the right countries would be especially important in this region.

- EMEA (Europe, Middle East, Africa): Often driven by energy and financials, but political risk, currency volatility, and geopolitical sensitivities can play a larger role. Investors should pay close attention to regional differences in EMEA, as shifts in resources, fiscal policy, and global trends can drive significant market movements.

Why China’s role within Emerging Markets is increasingly debated

China has traditionally made up a significant share of emerging market indices, but its role within EM has become more complex in recent years. Trade conflicts with the US, slower structural growth, and regulatory intervention are several factors that have led investors to reassess how China fits within a broader EM allocation.

At the same time, China remains the world’s second-largest economy. It is a key player in global manufacturing, supply chains, and is actively leading in sectors like renewable energy and electric vehicles. Thus, while China continues to be economically important, its market characteristics and policies increasingly diverge from those of other emerging economies.

As a result, the discussion for many investors has shifted: should China still be a part of a broader EM allocation, or treated separately as its own allocation?

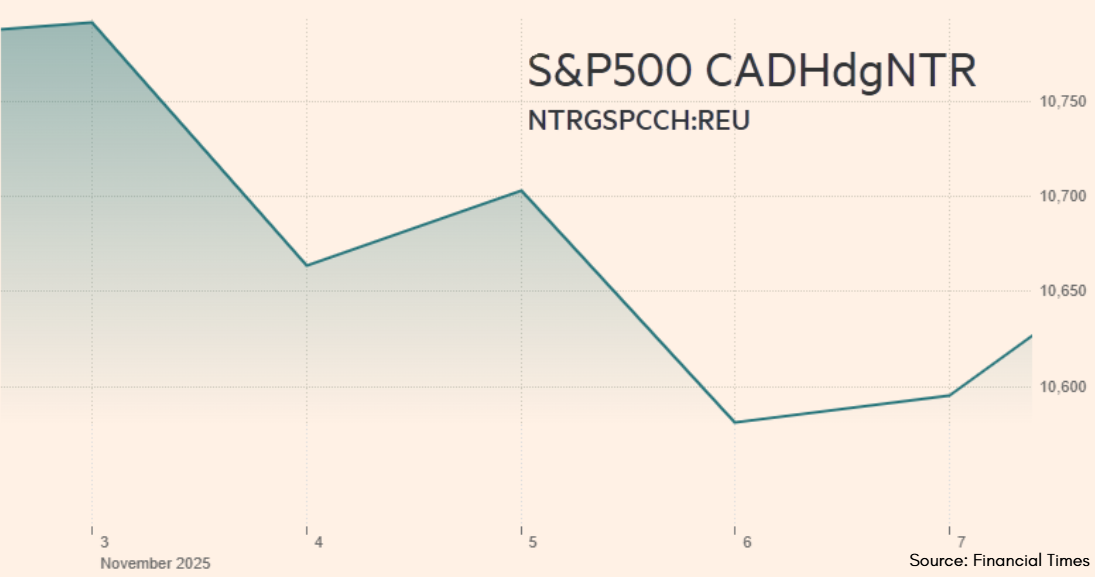

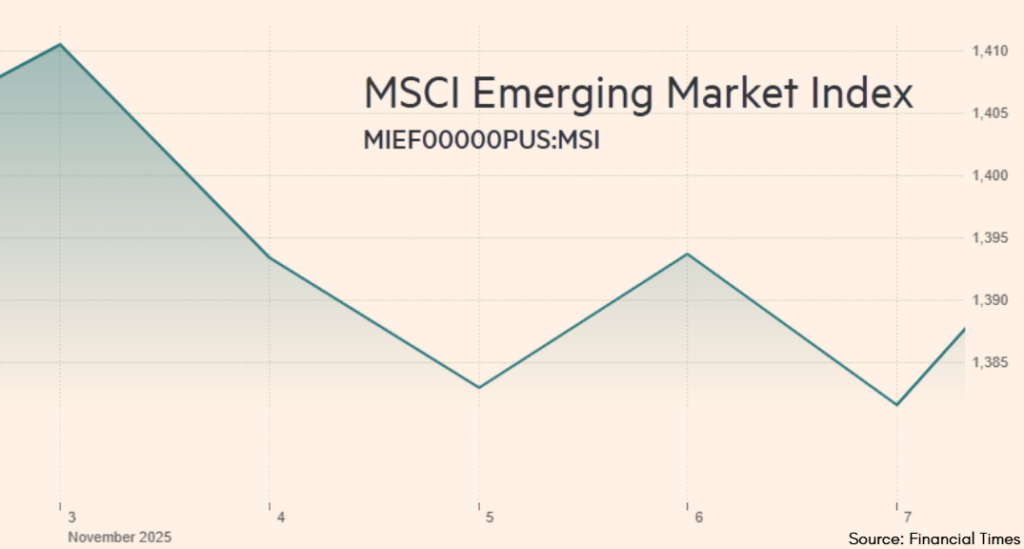

Case Study: November 2025 — China’s Break from the Pack

In the first week of November 2025, the S&P 500 fell as investors sold off high-priced tech and AI leaders, pushing the market into a broader risk-off move. Reuters attributed the decline to renewed concerns over valuations and the sustainability of the AI-driven rally, with heavy losses in semiconductors and mega-cap tech weighing on the index. The selloff was reinforced by macro uncertainty, including unpredictability around US fiscal policy and the government shutdown.

EM performance is typically highly sensitive to global financial conditions. As a result, broad EM indices often fall alongside global equities despite limited changes domestically.

Against this global backdrop, China was an exception: while most EM moved with global equities, China’s market strengthened over the period, marking a clear divergence from the general trend.

While a single case study is insufficient to settle the issue, it reinforces the broader debate explored in this article on whether China should still be classified alongside the rest of EM.

Products linked to Emerging Markets

Most investors continue to access EM through diversified UCITS funds, which are designed to provide broad, long-term exposure across regions and sectors, along with liquidity and risk management.

For instance, EM exposure within TEAM UCITS portfolios is usually kept measured rather than dominant. More conservative or balanced strategies tend to allocate only a small portion of the portfolio (~2-3%) to EM, while growth-oriented strategies may hold a higher allocation, though still controlled.

Therefore, while UCITS funds are often used for diversification, structured notes may be used selectively to target specific outcomes, such as income generation or risk protection. Ultimately, the two serve different purposes and are used in distinct ways depending on an investor’s objectives and risk tolerance.

Emerging markets are no longer a uniform asset group. Differences in regional dynamics and market structure mean that how exposure is gained now matters as much as the decision to allocate in the first place.

Written by Finna Ng