Investment Review 2nd Quarter 2026: Truce!

The second quarter of 2026 delivered one of the most powerful equity market recoveries in recent history, including a nine-week winning streak for the S&P 500. Yet the path there was anything but calm. Geopolitics and artificial intelligence dominated the narrative in almost equal measure, playing out against a backdrop of fragile investor sentiment as markets weighed an active conflict in the Middle East alongside growing scepticism over whether the enormous capital being poured into AI by the so-called “Hyperscalers” — Amazon, Google, Meta and Microsoft — would ever translate into meaningful profit.

After several false starts — including a brief reimposition of restrictions in the Strait of Hormuz by Iran, mutual accusations, and disagreement over the scope of any lasting settlement — the United States and Iran, with Pakistani mediation, ultimately reached an interim peace framework in June.

The Quarter in Numbers

It was a quarter of sharp contrasts across asset classes. Technology stocks led every sector with a 33.3% return, while equities broadly delivered double-digit gains across almost every major market. At the other extreme, energy fell 13.6% and oil prices collapsed, with Brent crude down over 38% and WTI down more than 31% for the quarter, as the worst fears around the Strait of Hormuz failed to materialise. Precious metals also had a torrid quarter, with silver down over 22% and gold down more than 14%, even as government bond markets stayed broadly resilient, led by a 3.9% gain in emerging market dollar debt.

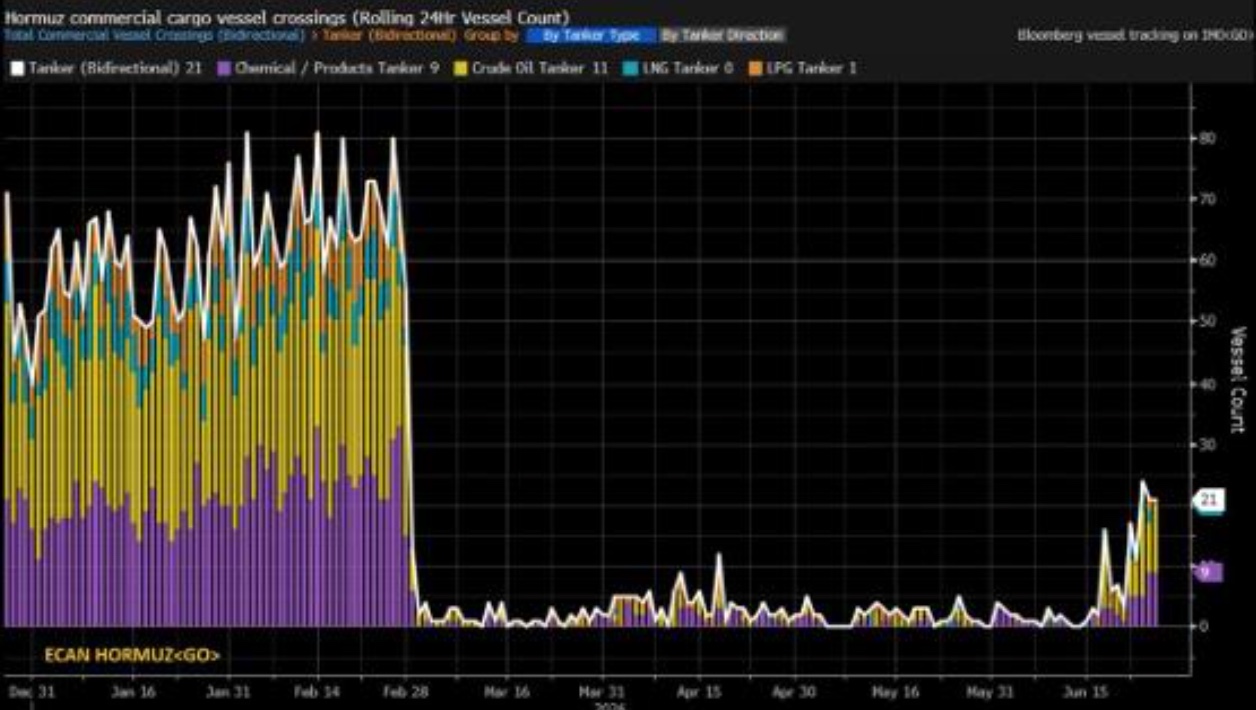

Oil Markets Breathe a Sigh of Relief

Chart: Bloomberg — Hormuz commercial tanker crossings, rolling 24-hour vessel count

The prospect of a fuller reopening of the Strait was met warmly by markets. Oil prices reversed course sharply, ending June below where they started before the conflict began — effectively pricing in a clean resolution to one of the largest geopolitical energy shocks on record, a shock that had removed more than a billion barrels of oil from the market through prolonged supply disruption.

Even so, the truce rests on a Memorandum of Understanding signed on 17 June — a preliminary, non-binding framework rather than a final treaty. Its terms include keeping the Strait open without external tolls or shipping charges, alongside a 60-day license permitting Iran to produce and sell oil to the US. Given how quickly earlier “deals” between the parties have unravelled, and Iran’s continuing leverage over the Strait, further disruption cannot be ruled out.

On the more constructive side, US refinery utilisation is running at multi-year highs, crude inventories sit at five-year lows, and strategic reserves around the world will need replenishing — commercial tanker traffic through the Strait has picked up meaningfully from its collapsed lows, though it remains at only around 20% of peak activity. Taken together, these factors argue against complacency on the downside for oil from here.

AI: Validation, For Now

With tensions in the Middle East cooling, investor attention swung back to first-quarter earnings season and, in particular, whether the AI investment cycle risks becoming one of the largest capital misallocations in history.

The scale of spending involved is striking. The four major hyperscalers are projected to spend a combined $800 billion on AI capital expenditure in 2027 alone, split largely across AI chips, data centre build-out, and the power infrastructure needed to run them. Capital expenditure as a share of these companies’ operating cash flow has more than doubled in three years, reaching an estimated 92% in 2026 — a level that leaves very little room for error if the anticipated returns on that spending don’t materialise.

Compounding the pressure, insatiable demand for AI compute has pushed prices of memory chips and AI “tokens” — the fragments of text, image or code that AI systems process and are billed by — sharply higher. There are early signs the cost is being passed down the chain: some businesses are reportedly shifting workloads away from expensive US cloud platforms toward cheaper alternatives, and Apple has already raised prices by $100–$300 across its Mac and iPad ranges, citing surging memory chip costs directly.

Two developments eased near-term concerns over the AI cycle, at least for now. The first was Anthropic’s announcement of Claude Mythos Preview, its most capable model to date, alongside Project Glasswing — an initiative applying the model to identify vulnerabilities across decades of operating system releases. The second, and arguably more market-moving, came from memory chip maker Micron Technology, whose blowout quarter — $41.4 billion in revenue and margins near 85%, equivalent to roughly $365 million of profit a day — served as a real-time health check on AI infrastructure demand and sent the broader semiconductor sector sharply higher.

Longer term, a new AI storyline may be emerging from China, where Hong Kong-listed Z.ai’s June release of its GLM 5.2 model represents a challenge to established US technology leadership that we believe remains under-appreciated by international investors — one with knock-on implications for memory chip demand more broadly.

A New Voice at the Federal Reserve

New Federal Reserve Chairman Kevin Warsh presided over his first policy meeting in mid-June. Rates were held at 3.50%–3.75%, but the accompanying language was notably more hawkish than under his predecessor, Jerome Powell — who had missed the Fed’s own inflation target for 63 consecutive months. Forward guidance was dropped, the policy statement was sharply shortened, and the tone shifted from signalling cuts to leaving hikes firmly on the table. Nine of eighteen FOMC participants now pencil in at least one hike for 2026, six of whom see two or more.

Warsh has also launched five internal task forces covering the Fed’s $6.7 trillion balance sheet, communications, data sources (including how inflation itself is measured), the labour market’s exposure to AI and technology, and inflation more broadly.

Sentiment softened somewhat toward month-end after core PCE inflation — the Fed’s preferred gauge — came in at 3.4% year-on-year for May, still well above target but better than markets had braced for. Money markets are now pricing in the possibility of up to two hikes over the next twelve months, up from expectations of cuts just a few months earlier.

A Political Shift Closer to Home

In the UK, former Manchester mayor Andy Burnham looks well placed to succeed Sir Keir Starmer as Prime Minister — the seventh change of UK leadership in under a decade. His platform includes bringing energy, housing, water and transport under greater public control, including the nationalisation of Thames Water. Markets, for now, remain unconvinced.

Equities: A Standout Quarter

Developed market equities, as measured by the MSCI World Index, returned 13.5% in sterling terms over the quarter. The S&P 500 returned 14.9%, while the technology-heavy Nasdaq climbed 21.3%.

Japan’s Nikkei 225 led global markets with a 33.8% return, buoyed by both the AI theme and Prime Minister Sanae Takaichi’s continued push for fiscal easing, including a proposed cut to consumption tax on food and beverages from April 2027.

Emerging markets also performed strongly, up 23.7%, as capital continued to flow toward the “picks and shovels” of the AI build-out — chiefly the memory chip makers of North Asia. Taiwan (now a $5.15 trillion market) and South Korea ($4.66 trillion) have risen to become the fifth and seventh largest equity markets in the world by capitalisation. China’s Shanghai market rose a more modest 6.6%, with investors largely looking past a record trade surplus and continued growth in intra-emerging-market trade, despite Beijing’s ongoing efforts to shift the economy’s centre of wealth creation away from property.

Fixed Income: Yields Ease, But Risks Remain

[Chart: Bloomberg/TEAM — UK, US and EU 10-year government bond yields, Q1–Q2 2026]

[Chart: Bloomberg/TEAM — UK, US and EU 10-year government bond yields, Q1–Q2 2026]

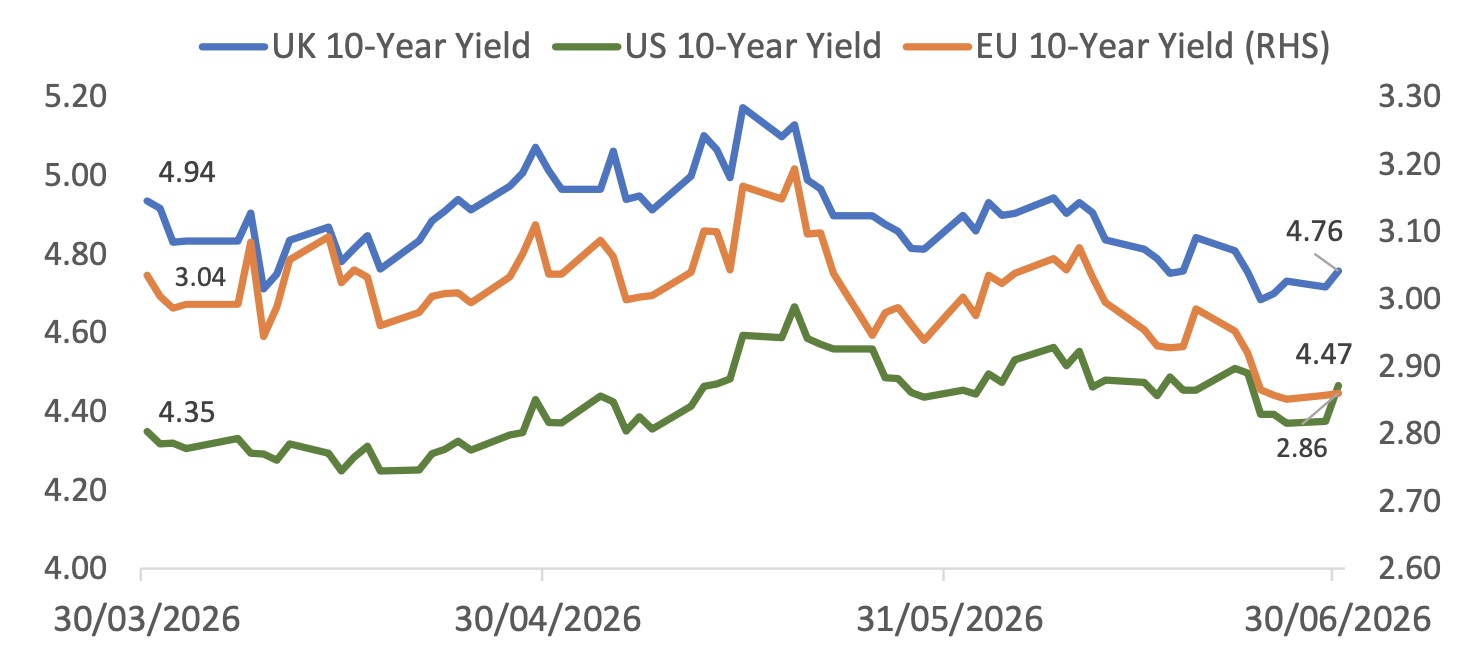

Government bond yields stayed elevated through April and May on fears that an extended Hormuz disruption would force central banks into hiking cycles. Record sovereign bond issuance — over $500 billion in the first half of the year, more than in the equivalent Covid-lockdown period of 2020 — added further pressure, with US debt-servicing costs now absorbing more than 19% of federal revenue, a 40-year high, as governments simultaneously boost military, infrastructure and household energy-support spending.

Yields eased in June as investors reassessed the odds of G7 rate hikes, helped by softer US jobs data and weaker growth readings across the UK and eurozone.

[Chart: Bloomberg/TEAM — Eurozone interest rate expectations, number of hikes/cuts vs implied rate]

[Chart: Bloomberg/TEAM — Eurozone interest rate expectations, number of hikes/cuts vs implied rate]

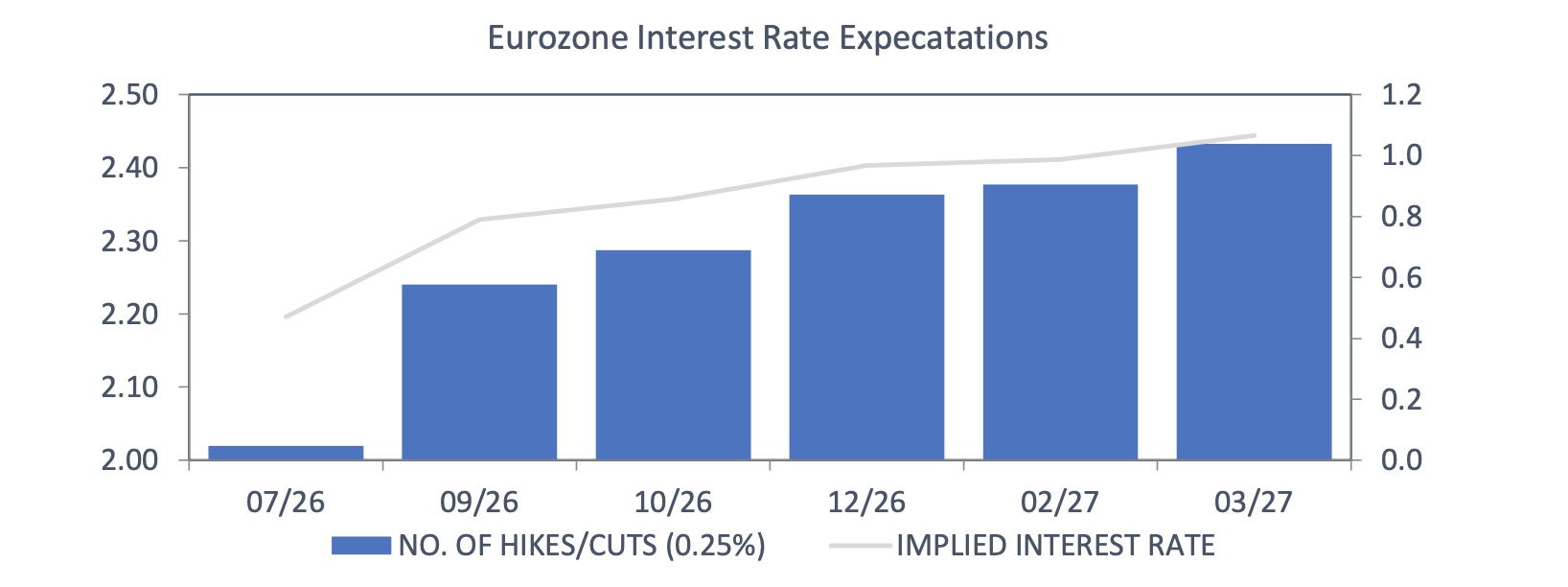

The European Central Bank raised its deposit rate a quarter point to 2.25% — its first hike since 2023 and a sharp reversal after eight consecutive cuts between mid-2024 and mid-2025 — as flash eurozone inflation hit 3.2% in May and core inflation rose to 2.5%. President Lagarde was careful to note this was not a one-off “insurance” move, though June’s subsequent fall in headline inflation to 2.8% (and core to 2.4%) has since split opinion within the Governing Council, with Chief Economist Philip Lane cautioning that wage and price pressures unleashed by the conflict are still working their way through the system.

[Chart: Bloomberg/TEAM — UK interest rate expectations, number of hikes/cuts vs implied rate]

[Chart: Bloomberg/TEAM — UK interest rate expectations, number of hikes/cuts vs implied rate]

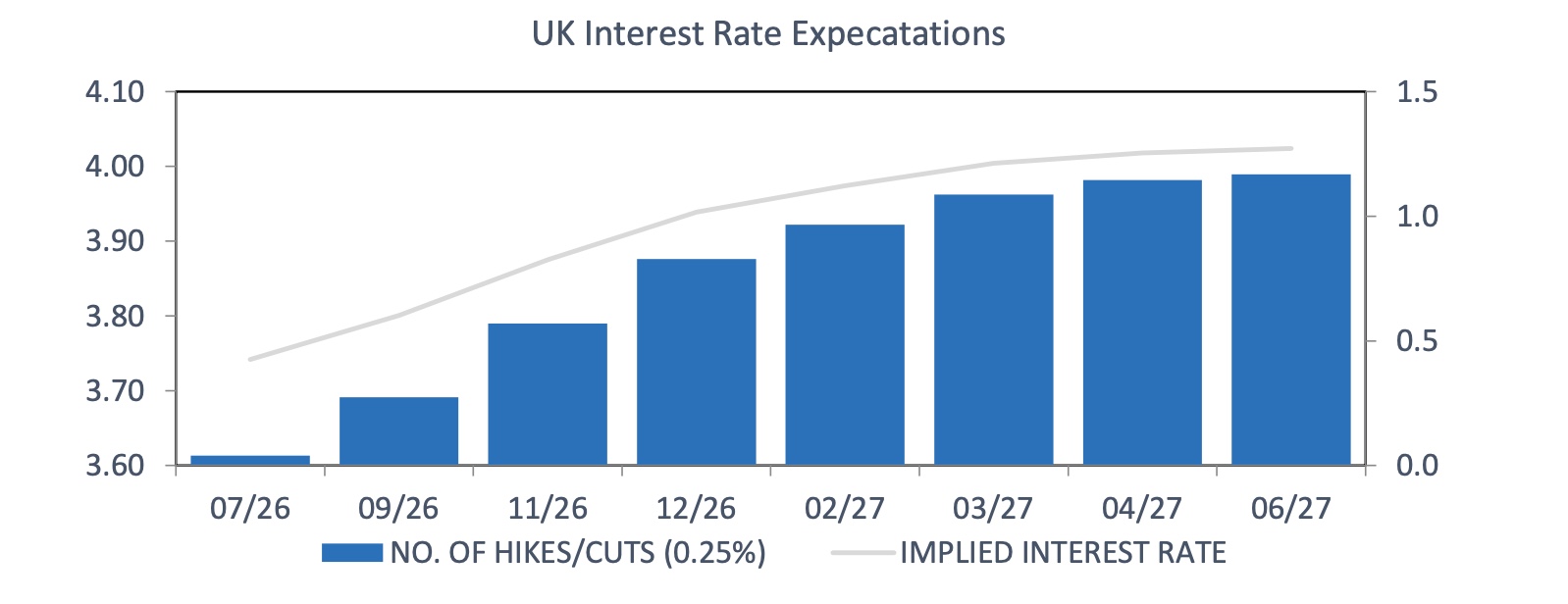

The Bank of England held rates at 3.75% on a 7–2 vote, balancing still-high inflation — the highest in the G7 — against disappointing growth. The UK economy is forecast to expand just 0.6% in the first half of 2026, with unemployment at its highest level since the pandemic. A minority on the committee, including chief economist Huw Pill, pushed for an immediate rate rise; the majority, including Governor Andrew Bailey, judged the weaker growth backdrop the greater risk.

Notably, at the ECB’s Sintra forum, Lagarde, Bailey and the Bank of Canada’s Tiff Macklem all signalled a broader shift away from firm forward guidance toward what Lagarde termed “framework guidance” — explaining how decisions will be made, rather than pre-committing to a path — reflecting how supply shocks and geopolitical uncertainty have made rate forecasting a riskier exercise for central banks generally.

Commodities: A Reversal in Fortune

Oil and gas prices fully retraced their first-quarter spike as markets priced in normalised Hormuz operations. Gold and silver, by contrast, lost their shine over the quarter — pressured by a combination of cash-strapped central banks becoming forced sellers, rising real bond yields offering an attractive alternative, and the unwinding of leveraged ETF and retail positioning built up earlier in the year. Silver’s dual role as both a precious and industrial metal made it additionally vulnerable to periodic growth scares. Precious metals mining equities followed suit, squeezed by both lower spot prices and stubbornly high wage and energy costs, with the sector’s earlier institutional rally also making it a natural source of profit-taking to fund opportunities elsewhere.

Separately, US public finances remain under strain: roughly 93% of existing US interest payments are directed to Medicare, Medicaid and Social Security — effectively untouchable — and the national debt grew by close to $280 billion over the quarter despite a bumper tax-revenue season, underscoring the scale of the long-term fiscal challenge facing policymakers.

Positioning for the Third Quarter

What worked in Q2 2026: US mega-cap technology stocks, South Korean and Taiwanese equities, value-oriented global equities, US infrastructure equities, and Japanese equities.

What didn’t: commodities broadly, including physical gold, precious metals mining stocks, and energy equities, along with cash and ultra-short duration government bonds.

Heading into Q3 2026, our preferred approach continues to pair US mega-cap technology exposure with ex-US markets tied to the AI supply chain — notably Samsung Electronics, SK Hynix, and TSMC — alongside a continued overweight to Japan. Across our tactical asset allocation, we remain overweight US large cap and broadly neutral on global technology, while staying underweight global small cap.

In fixed income, we favour a combination of ultra-short government bonds and quality investment-grade credit focused on the “belly” of the curve — less exposed to long-end volatility while still able to benefit from steeper credit curves. Credit spreads remain historically tight, so while we don’t see an immediate catalyst for meaningful widening, careful credit and sector selection matters more than it has in recent years.

Within our liquid alternatives allocation, our framework continues to point to real assets becoming more attractive against a backdrop of tightening global supply and resilient demand — a view that also supports our stance on silver and geared precious metals miners over the longer term, even after this quarter’s weakness.

Elevated volatility and rising cross-asset correlation have also led us to hold healthy cash levels within our lower and medium-risk mandates, with a view to redeploying into risk assets as clearer opportunities emerge over the summer months.

As ever, rather than attempting to predict individual events, we rely on a disciplined, systematic investment process — one that has navigated a wide range of market conditions through this post-pandemic cycle and continued to deliver risk-adjusted returns for our clients.

At NEBA Financial Solutions, we believe navigating quarters like this one is exactly where an experienced, risk-aware approach earns its keep — helping advisers and their clients look past short-term noise and stay focused on long-term, defined outcomes.

Source: adapted from TEAM Weekly Commentary, Craig Farley, Chief Investment Officer, July 2026.