Quick question:

Which Structured Note do you think carries more risk?

At first glance, one structure may appear riskier than the other.

In reality, both involve risk — just in different forms.

To understand why, it is necessary to move beyond a single definition of risk and consider two distinct dimensions: risk to capital and risk to return. Structured Notes provide a useful framework for examining this distinction.

Understanding Risk in Investing:

Risk to Capital vs Risk to Return Through Structured Notes

Risk is one of the most frequently referenced concepts in investment discourse, yet it is often discussed in simplified or imprecise terms. In many investor conversations, risk is implicitly reduced to a single question: whether capital may be lost. While capital preservation is clearly an important consideration, focusing solely on this dimension risks overlooking a second, distinct aspect of investment uncertainty — namely, the possibility that an investment may fail to generate the anticipated return, even in the absence of capital loss.

Structured Notes may provide a useful framework for examining this distinction. By design, they can separate risk to capital from risk to return and specify how each may behave under predefined market conditions. In doing so, Structured Notes can assist advisers in articulating investment trade-offs more clearly and in framing discussions around expected outcomes with greater precision.

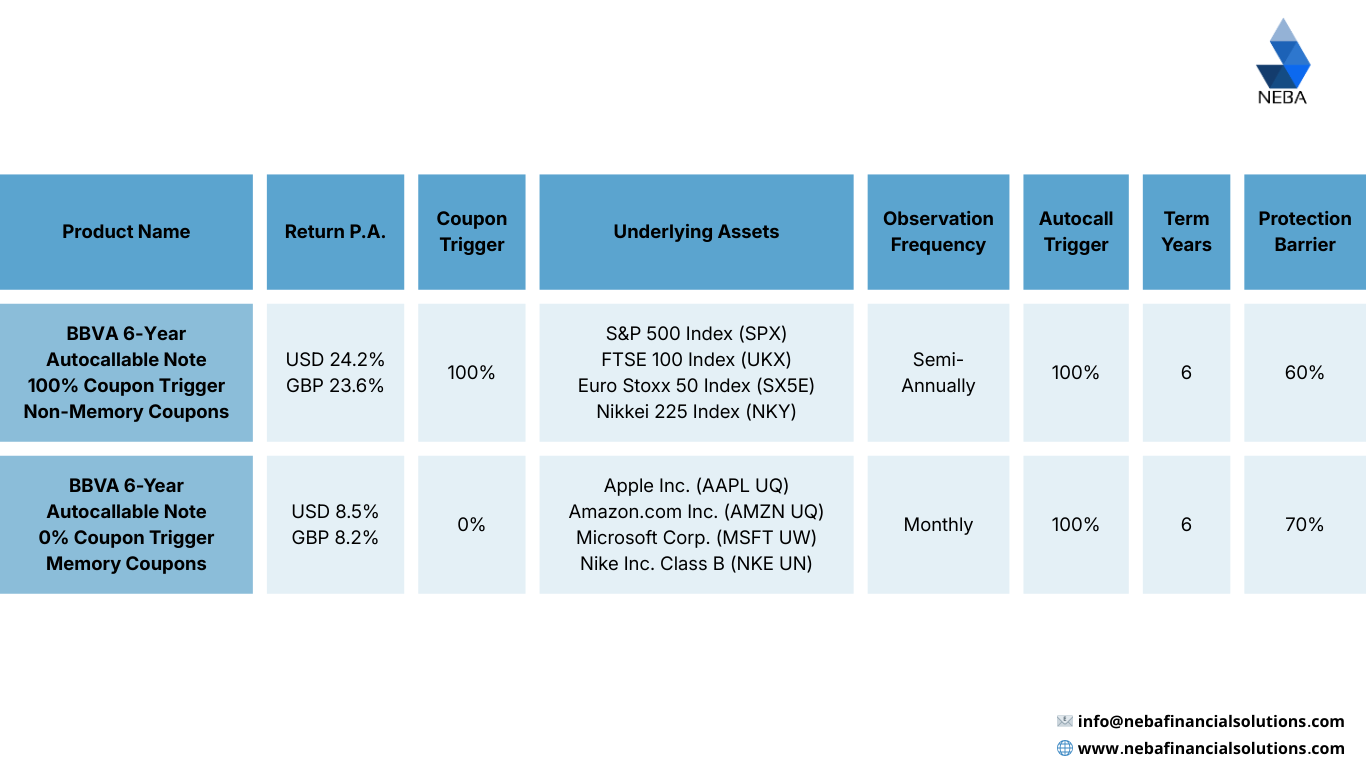

Risk to capital refers to the potential for partial or total loss of the invested principal. In the context of Structured Notes, this risk is typically associated with two primary factors: the performance of the underlying asset relative to a predefined protection barrier, and the creditworthiness of the issuing institution. Where the underlying asset remains above the protection barrier at maturity, the return of capital is generally expected, subject to issuer solvency. Conversely, if the underlying breaches the barrier, capital losses may occur in proportion to the decline in the underlying asset. Importantly, these scenarios are defined at inception, such that the conditions under which capital may be at risk are known in advance rather than left open-ended.

Risk to return, by contrast, concerns the uncertainty surrounding income generation or capital growth. Many Structured Notes are designed to offer enhanced coupons or yield; however, such returns are commonly conditional rather than guaranteed. Coupon payments are typically linked to the performance of the underlying asset relative to predefined trigger levels on scheduled observation dates. Where these conditions are not met, coupons may not be paid, notwithstanding the preservation of capital. This distinction is not always well understood, particularly where investors equate capital protection with overall investment success.

Autocall features further illustrate how Structured Notes may shape return outcomes. An autocall provision allows a Structured Note to redeem prior to its final maturity if specified performance conditions are satisfied. When triggered, the investor typically receives the return of principal along with any accrued coupon. Such features may be advantageous in stable or rising market environments, as they enable returns to be realised earlier than initially anticipated. At the same time, early redemption introduces reinvestment risk, as capital may be returned at a time when comparable opportunities are less readily available or less attractive.

The underlying asset plays a central role in determining all Structured Note outcomes. Whether linked to a single equity, an index, or a basket of assets, the performance of the underlying influences coupon payments, the likelihood of early redemption, and the application of capital protection mechanisms. Accordingly, the selection of appropriate underlyings represents a key consideration in aligning Structured Notes with an investor’s objectives, risk tolerance, and broader portfolio context.

One feature that distinguishes Structured Notes from many traditional investment instruments is their capacity to define potential outcomes in advance rather than relying solely on directional market exposure. Instead of being simultaneously exposed to both capital and return risk in an unconstrained manner, investors may, within defined parameters, choose which risks they are prepared to accept. Some investors may prioritise capital preservation and accept conditional or uncertain returns, while others may be willing to tolerate defined downside risk in exchange for higher potential income or yield.

This degree of flexibility also suggests that Structured Notes may be designed rather than merely selected. With appropriate professional guidance, investors may choose underlyings they understand, determine protection levels consistent with their risk preferences, and structure return profiles aligned with income or growth objectives. In this respect, Structured Notes may shift the investment discussion from product selection toward outcome specification.

For advisers, the role is not to emphasise structural complexity, but to promote clarity and suitability. Structured Notes require careful explanation, thorough assessment of client circumstances, and appropriate integration within a diversified portfolio. When used judiciously and with full consideration of their risks and limitations, they may support more tailored financial solutions than those offered by generic market exposures.

Ultimately, investment risk cannot be reduced to a single dimension. A more complete understanding requires consideration of how both capital and returns may behave under different conditions. Structured Notes make these distinctions explicit, thereby supporting more informed, objective, and disciplined investment discussions between advisers and clients.

Written by Yiyi Chen